(all amounts in US dollars, unless otherwise noted)

Vancouver, British Columbia – Ero Copper Corp. (TSX: ERO) (“Ero” or the “Company”) today is pleased to announce its financial results for the three and nine-months ended September 30, 2019. Management will host a conference call tomorrow, Wednesday, November 6, 2019, at 11:30 a.m. Eastern to discuss the results. Dial-in details for the call can be found near the end of this press release.

HIGHLIGHTS

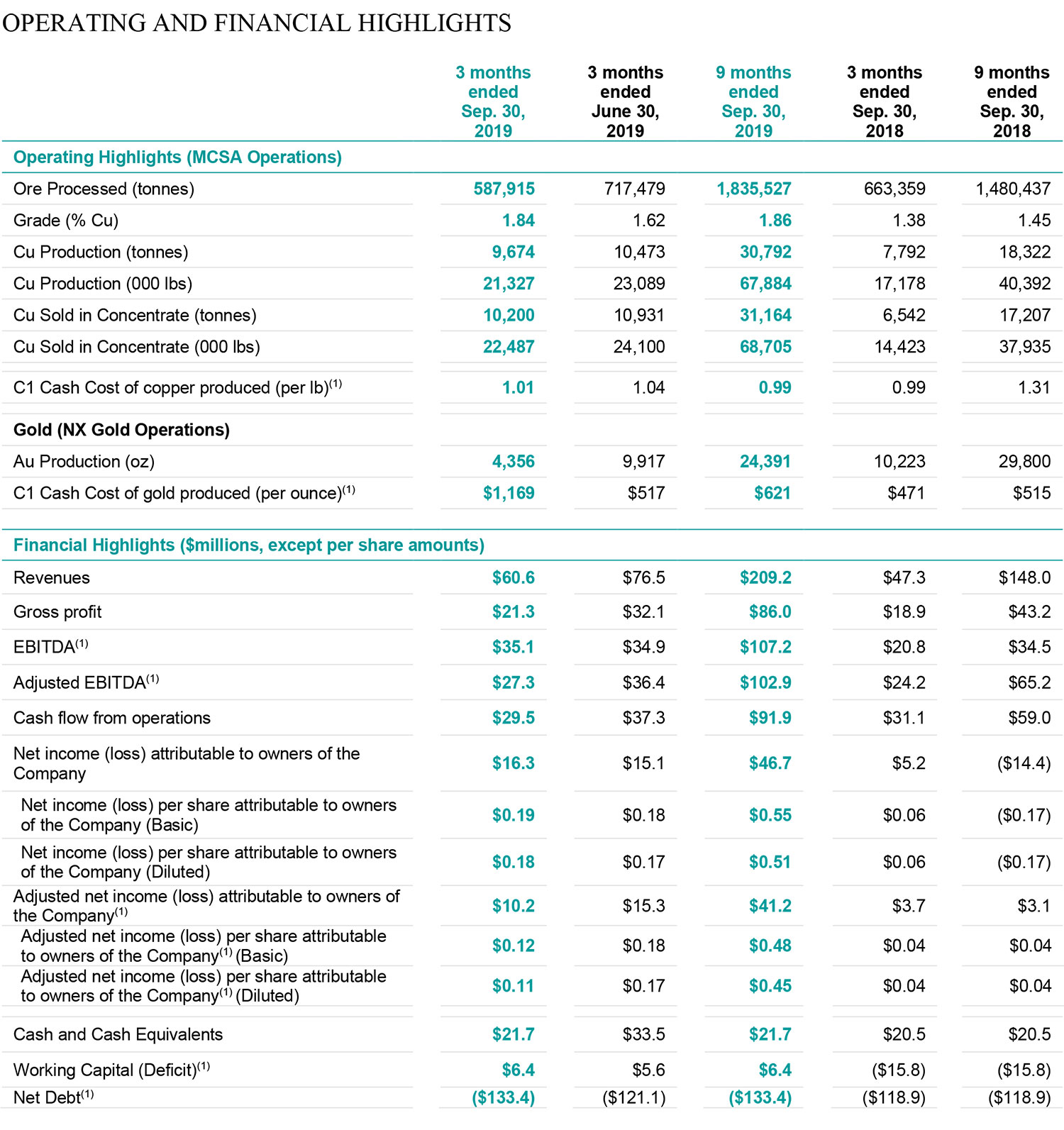

- Third quarter copper production of 9,674 tonnes of copper resulting in 30,792 tonnes of total copper produced year-to-date in 2019;

- C1 cash costs* of $1.01 and $0.99 per pound of copper produced during the three and nine-month period ended September 30, 2019, respectively;

- Generated $27.3 and $102.9 million in Adjusted EBITDA* and $29.5 and $91.9 million in cash flow from operations during the three and nine-month period ended September 30, 2019, respectively;

- Net income attributable to owners of the Company of $16.3 and $46.7 million ($0.18 and $0.51 per share on a diluted basis) during the three and nine-month period ended September 30, 2019; respectively;

- Adjusted net income attributable to owners of the Company* of $10.2 and $41.2 million ($0.11 and $0.45 per share on a diluted basis) during the three and nine-month period ended September 30, 2019, respectively;

- Transitional quarter at the NX Gold Mine with 4,356 ounces of gold produced at C1 cash costs* of $1,169 per ounce as the last exposed ore within the Brás vein was mined and development of the new Santo Antonio vein advanced in preparation for mining in the fourth quarter. Year-to-date production totalled 24,391 ounces of gold at C1 cash costs* of $621 per ounce;

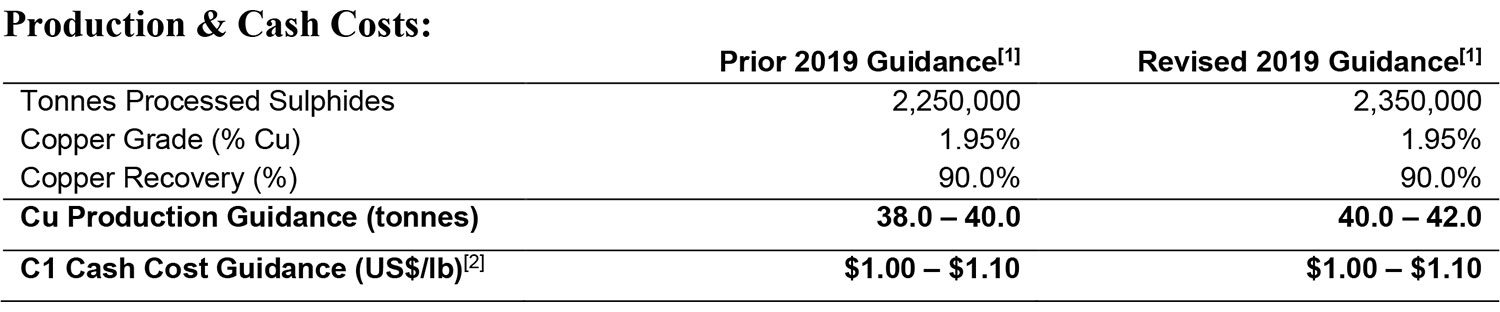

- Increase full-year copper production guidance outlook for 2019 by an additional 2,000 tonnes of copper to between 40,000 and 42,000 tonnes and reiterate C1 cash cost* guidance range for the full year to be at the low-end of the Company’s guidance range, between $1.00 and $1.10 per pound of copper produced. At NX Gold, the Company expects an improved operating outlook for fourth quarter of 2019, forecasting approximately 7,500 ounces of gold production at C1 cash costs* of approximately $700 per ounce.

Commenting on the results, David Strang, President and CEO, stated, “During the third quarter we saw continued strong operating performance at MCSA. Based upon this performance, we are increasing copper production guidance again for the full year. This increase is, in part, driven by the outstanding contribution of the Vermelhos mine. Looking forward, we anticipate grades processed during the fourth quarter to increase resulting in a blended full-year mill head-grade of approximately 1.95% copper.

At our NX Gold Mine, the decline in production during the third quarter occurred as we concluded mining activities within the Brás vein and advanced development into the newly discovered Santo Antonio vein in preparation for mining in the fourth quarter. Based on drilling to date, we see multiple years of mine life from Santo Antonio, with additional exploration upside, as well as elevated production levels, at low cost, commencing in the fourth quarter of this year. An updated National Instrument 43-101 compliant mineral resource and reserve estimate, detailing these plans will be announced prior to year end.

On the corporate side, our finance and legal teams continue to deliver accretive results for the Company. During the period, MCSA was notified of a favourable court ruling which confirmed MCSA’s outstanding claim to a historic tax credit related to prior overpayment resulting in the Company formally recognizing an R$89.9 million (approximately $22 million) tax credit, that will be used to offset future taxes payable in 2020 and 2021.

On exploration, our drill programs are primarily focused on the investigation of high-priority regional exploration targets throughout the Curaçá Valley.”

*EBITDA, Adjusted EBITDA, Adjusted net income (loss), C1 cash cost of copper produced (per lb) and C1 cash costs of gold produced (per ounce) are non-IFRS measures – see the Notes section of this press release for a discussion on non-IFRS Measures

OPERATIONS & EXPLORATION HIGHLIGHTS

- Mining & Milling Operations – continued strong performance in 2019 at MCSA and improved full year guidance

- 587,915 tonnes of ore grading 1.84% copper processed during the third quarter producing 9,674 tonnes of copper in concentrate after metallurgical recoveries of 89.2%.

- Total of 1.8 million tonnes of ore processed grading 1.86% copper producing 30,792 tonnes of copper in concentrate after metallurgical recoveries that averaged 90.4% during the nine-month period ended September 30, 2019.

- Strong operating performance from Vermelhos, highlighted by a significant quarter-on-quarter increase in grades mined with 176,183 tonnes grading 3.84% copper mined during the period – a 56% increase in grade compared to the prior period.

- Total Vermelhos production of 492,122 tonnes of ore grading 3.43% copper mined during the nine-month period ended September 30, 2019.

- As a result of transitioning mining activities from the Brás vein into the new Santo Antonio vein, the Company’s 97.6% owned NX Gold Mine processed 34,813 tonnes of ore grading 4.51 grams per tonne gold during the period, producing 4,356 ounces of gold and 2,909 ounces of silver as by-product after metallurgical recoveries that averaged 86.2% during the third quarter of 2019.

- Total of 115,068 tonnes of ore grading 7.23 grams per tonne gold processed producing 24,391 ounces of gold and 15,326 ounces of silver after metallurgical recoveries that averaged 91.2% during the nine-month period ended September 30, 2019.

- Expect a production rebalance to commence in the fourth quarter with approximately 7,500 ounces of gold production forecast during the period, resulting in total 2019 production of approximately 32,000 ounces gold.

- 587,915 tonnes of ore grading 1.84% copper processed during the third quarter producing 9,674 tonnes of copper in concentrate after metallurgical recoveries of 89.2%.

- Exploration Activities – shift in focus to regional exploration targets

- Vermelhos District

- Regional greenfield drilling within the Vermelhos District, where 15 drill rigs are operating (one additional rig on year end maintenance), is currently targeting several high-priority exploration targets identified during the Company’s comprehensive targeting work. These targets extend over approximately 10 kilometers of anomalous soil geochemistry and induced polarization (“IP”) anomalies.

- Pilar District

- Exploration activity within the Pilar District, where 10 drill rigs are currently operating (one additional rig on year end maintenance), continues to focus on infill and extensional drilling of high-grade zones that the Company has yet to fully delineate within the Pilar underground mine. These zones are highlighted by recent drill results from the Deepening zone, located down-plunge to the north and along strike to the south of known mineralization. In addition, drilling at Pilar will seek to further delineate the area surrounding recent results in the South Extension zone, which is located at higher levels of the mine south of the planned mining blocks of MSB South.

- NX Gold Mine

- At the NX Gold Mine, three exploration drill rigs are currently operating on extensions of the recently announced Santo Antonio vein and testing for continuity of the Brás vein. Additionally, the first comprehensive regional exploration program is underway.

- Vermelhos District

- Corporate Highlights – Unlocking value with resolution of historic tax credit and strong overall liquidity at quarter end

- During the third quarter, the Company successfully recognized an outstanding claim of a historic tax credit, totalling R$89.9 million (approximately $22 million), related to prior overpayment. This credit is expected to offset future taxes payable in 2020 and 2021.

- As at the end of the quarter, the Company had a total cash position of $23.6 million (including restricted cash) plus $14.0 million undrawn on its secured, revolving credit facility in Canada and an additional R$77.5 million in available undrawn lines of credit in Brazil.

OPERATING AND FINANCIAL HIGHLIGHTS

Footnotes

[1] EBITDA, Adjusted EBITDA, Adjusted net income (loss), Adjusted net income (loss) per share, Net Debt, Working Capital, C1 cash cost of copper produced (per lb) and C1 cash cost of gold produced (per ounce) are non-IFRS measures – see the Notes section of this press release for a discussion on non-IFRS Measures

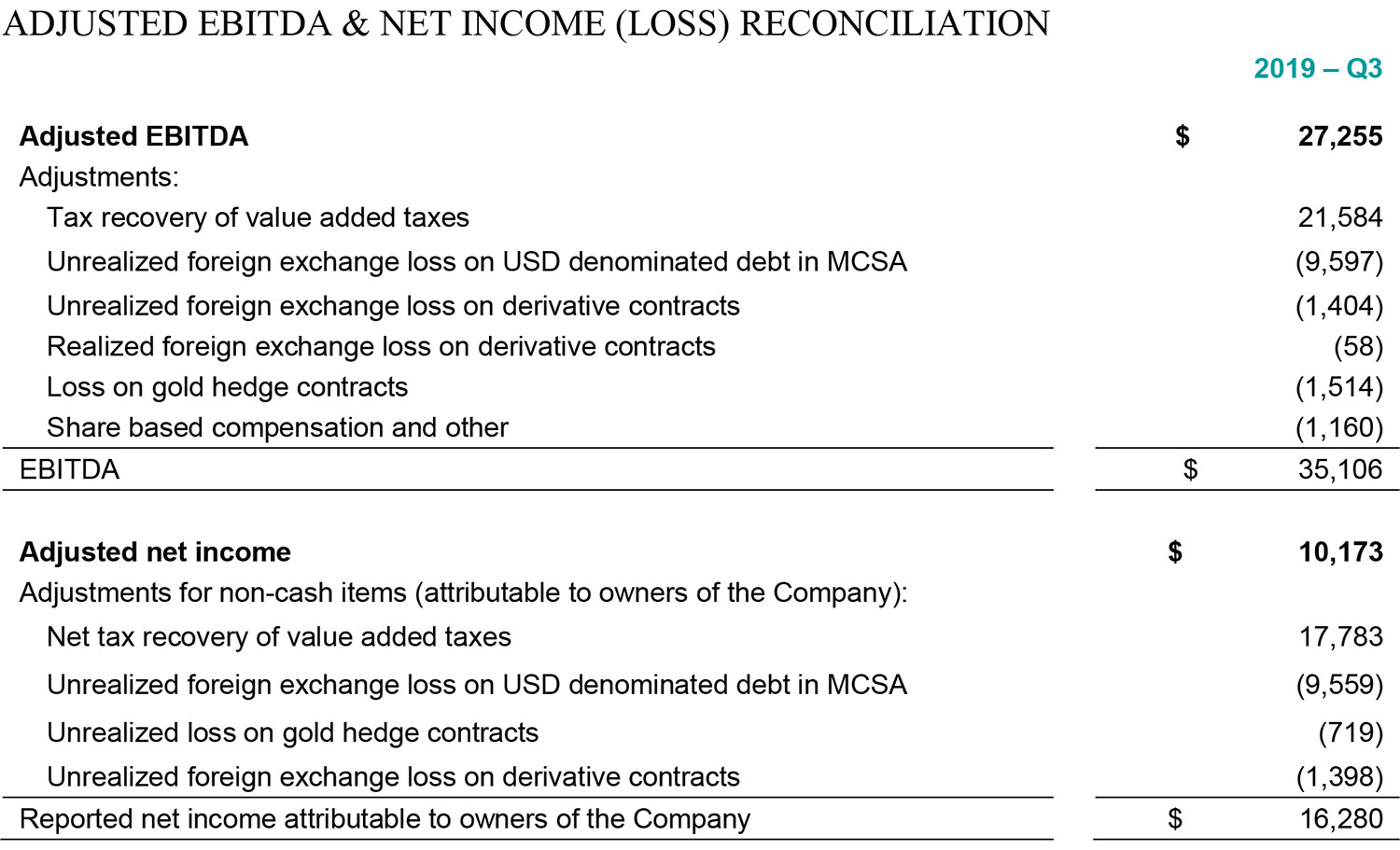

ADJUSTED EBITDA & NET INCOME (LOSS) RECONCILIATION

OUTLOOK

Based upon strong operational performance to date, the Company is updating its copper production and capital expenditure guidance for 2019. While the C1 cash cost guidance range remains unchanged, due to improved production outlook and favorable prevailing foreign exchange rates, the Company expects full year C1 cash costs to fall at the low-end of the guidance range, around $1.00 per pound of copper produced.

Production & Cash Costs:

Footnotes:

[1] Guidance is based on certain estimates and assumptions, including but not limited to, mineral reserve estimates, grade and continuity of interpreted geological formations and metallurgical performance. Please refer to the Company’s SEDAR filings for complete risk factors.

[2] C1 cash costs of copper produced (per lb.) is a non-IFRS measures – see the Notes section of this press release for a discussion of non-IFRS measures.

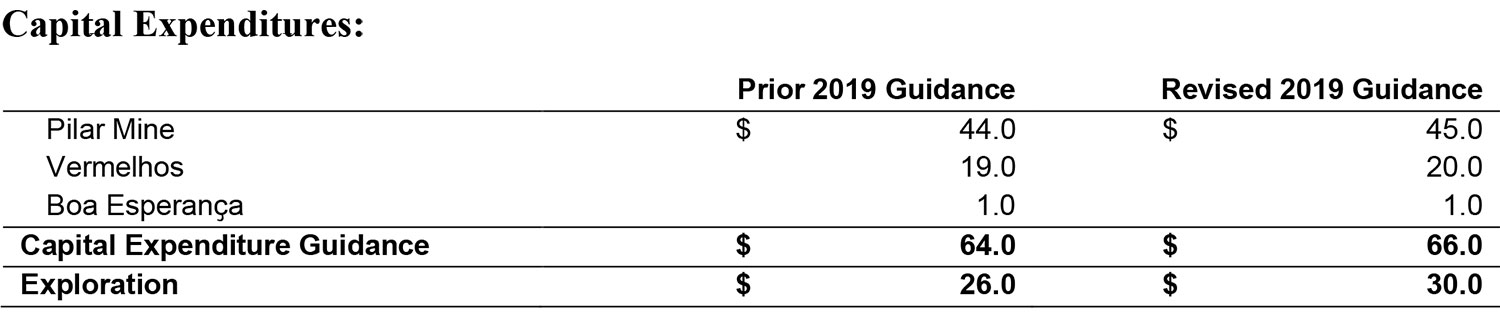

Capital Expenditures:

The Company’s revised capital expenditure guidance for 2019 assumes a USD:BRL foreign exchange rate of 3.90 (previous guidance assumed a USD:BRL foreign exchange rate of 3.80) and has been presented below in USD millions.

Revised capital expenditure guidance reflects increased exploration expenditures, with the Company now expecting to drill approximately 220,000 meters by year-end, as well as on additional development at the Pilar and Vermelhos mines to enhance operational flexibility and production volumes in 2019 and 2020. In addition, delivery of a 200,000 tonne per annum ore sorting plant, purchased in the third quarter, is underway. The plant is expected to be commissioned during the fourth quarter of 2019.

NOTES

Non-IFRS measures

- Financial results of the Company are prepared in accordance with IFRS. The Company utilizes certain non-IFRS measures, including C1 cash cost of copper produced (per lb), C1 cash costs of gold produced (per ounce), EBITDA, Adjusted EBITDA, Adjusted net income (loss), Adjusted earnings (loss) per share, net debt and working capital, which are not measures recognized under IFRS. The Company believes that these measures, together with measures determined in accordance with IFRS, provide investors with an improved ability to evaluate the underlying performance of the Company. Non-IFRS measures do not have any standardized meaning prescribed under IFRS, and therefore they may not be comparable to similar measures employed by other companies. The data is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

C1 cash cost of copper produced (per lb.)

- C1 cash cost of copper produced (per lb) is the sum of production costs, net of capital expenditure development costs and by-product credits, divided by the copper pounds produced. C1 cash costs reported by the Company include treatment, refining charges, offsite costs, and certain tax credits relating to sales invoiced to the Company’s Brazilian customer on sales. By-product credits are calculated based on actual precious metal sales (net of treatment costs) during the period divided by the total pounds of copper produced during the period. C1 cash cost of copper produced per pound is a non-IFRS measure used by the Company to manage and evaluate operating performance of the Company’s operating mining unit, and is widely reported in the mining industry as benchmarks for performance, but does not have a standardized meaning and is disclosed in addition to IFRS measures.

C1 cash cost of gold produced (per ounce)

- C1 cash cost of gold produced (per ounce) is the sum of production costs, net of capital expenditure development costs and silver by-product credits, divided by the gold ounces produced. By-product credits are calculated based on actual precious metal sales during the period divided by the total ounces of gold produced during the period. C1 cash cost of gold produced per pound is a non-IFRS measure used by the Company to manage and evaluate operating performance of the Company’s operating mining unit and is widely reported in the mining industry as benchmarks for performance but does not have a standardized meaning and is disclosed in addition to IFRS measures.

Earnings before interest, taxes, depreciation and amortization (EBITDA) and Adjusted EBITDA

- EBITDA represents earnings before interest expense, income taxes, depreciation, and amortization. Adjusted EBITDA includes further adjustments for non-recurring items and items not indicative to the future operating performance of the Company. The Company believes EBITDA and adjusted EBITDA are appropriate supplemental measures of debt service capacity and performance of its operations.

Adjusted EBITDA is calculated by removing the following income statement items:- Tax recovery of value added taxes

- Loss on debt settlement

- Foreign exchange loss

- Loss on gold hedge contracts

- Share based compensation

Adjusted Net Income (Loss) and Adjusted Earnings (Loss) Per Share

- The Company uses the financial measure “Adjusted net income (loss)” and “Adjusted earnings (loss) per share” to supplement information in its consolidated financial statements. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, the Company and certain investors and analysts use this information to evaluate the Company’s performance. The Company excludes non-cash and unusual items from net earnings to provide a measure which allows the Company and investors to evaluate the operating results of the underlying core operations.

During the period, the following non-cash or unusual adjustments to calculated adjusted net income (loss):- Net tax recovery of value added taxes

- Loss on debt settlement

- Unrealized foreign exchange loss on USD denominated debt in MCSA

- Unrealized loss on gold hedge contracts

- Unrealized foreign exchange loss on foreign exchange derivatives contract

Net Debt

- Net debt is determined based on cash and cash equivalents, restricted cash and loans and borrowings as reported in the Company’s consolidated financial statements. The Company uses net debt as a measure of the Company’s ability to pay down its debt.

Working capital

- Working capital is determined based on current assets and current liabilities as reported in the Company’s consolidated financial statements. The Company uses working capital as a measure of the Company’s short-term financial health and operating efficiency.

CONFERENCE CALL DETAILS

The Company will hold a conference call on Wednesday, November 6, 2019 at 11:30 am Eastern time (8:30 am Pacific time) to discuss these results.

| Date: | Wednesday, November 6, 2019 |

| Time: | 11:30 am Eastern time (8:30 am Pacific time) |

| Dial in: | North America: 1-800-319-4610, International: +1-604-638-5340 please dial in 5-10 minutes prior and ask to join the call |

| Replay | North America: 1-800-319-6413, International: +1-604-638-9010 |

| Replay Passcode: | 3784 |

This press release should be read in conjunction with the unaudited condensed consolidated interim financial statements and management’s discussion and analysis (“MD&A”) for the three and nine-month periods ended September 30, 2019 available on the Company’s website www.erocopper.com and on SEDAR (www.sedar.com).

ABOUT ERO COPPER CORP

Ero Copper Corp, headquartered in Vancouver, B.C., is focused on copper production growth from the Vale do Curaçá Property, located in Bahia, Brazil. The Company’s primary asset is a 99.6% interest in the Brazilian copper mining company, Mineração Caraíba S.A. (“MCSA”), 100% owner of the Vale do Curaçá Property with over 40 years of operating history in the region. The Company currently mines copper ore from the Pilar and Vermelhos underground mines. In addition to the Vale do Curaçá Property, MCSA owns 100% of the Boa Esperanҫa development project, an IOCG-type copper project located in Pará, Brazil and the Company, directly and indirectly, owns 97.6% of the NX Gold Mine, an operating gold and silver mine located in Mato Grosso, Brazil. Additional information on the Company and its operations, including technical reports on the Vale do Curaçá, Boa Esperanҫa and NX Gold properties, can be found on the Company’s website (www.erocopper.com) and on SEDAR (www.sedar.com).

Rubens Mendonça, MAusIMM, Chartered Professional – Mining, has reviewed and approved the scientific and technical information contained in this press release. Mr. Mendonça is a Qualified Person and is independent of Ero as defined by National Instrument 43-101, Standards of Disclosure for Mineral Projects (“NI 43-101”).

| ERO COPPER CORP. | |

| Signed: “David Strang” | For further information contact: |

| David Strang, President & CEO | Makko DeFilippo, Vice President, Corporate Development |

| (604) 429-9244 | |

| info@erocopper.com | |

CAUTION REGARDING FORWARD LOOKING INFORMATION AND STATEMENTS This Press Release contains “forward-looking information” within the meaning of applicable Canadian securities laws. Forward-looking information includes statements that use forward-looking terminology such as “may”, “could”, “would”, “will”, “should”, “intend”, “target”, “plan”, “expect”, “budget”, “estimate”, “forecast”, “schedule”, “anticipate”, “believe”, “continue”, “potential”, “view” or the negative or grammatical variation thereof or other variations thereof or comparable terminology. Such forward-looking information includes, without limitation, statements with respect to the Company's expected operations at the Vermelhos and Pilar Mines as well as at the NX Gold Property, drilling plans, plans for the Company's exploration program, timing of any updated mineral resource and reserve updates and technical reports, the Company's future production outlook, cash costs, capital resources and expenditures and the expected timeframe to use tax credits to offset future taxes payable by MCSA.

Forward-looking information is not a guarantee of future performance and is based upon a number of estimates and assumptions of management in light of management’s experience and perception of trends, current conditions and expected developments, as well as other factors that management believes to be relevant and reasonable in the circumstances, as of the date of this Press Release including, without limitation, assumptions about: favourable equity and debt capital markets; the ability to raise any necessary additional capital on reasonable terms to advance the production, development and exploration of the Company’s properties and assets; future prices of copper and other metal prices; the timing and results of exploration and drilling programs; the accuracy of any mineral reserve and mineral resource estimates; the geology of the Vale do Curaçá Property, NX Gold Mine and the Boa Esperanҫa Property being as described in the technical reports for these properties; production costs; the accuracy of budgeted exploration and development costs and expenditures; the price of other commodities such as fuel; future currency exchange rates and interest rates; operating conditions being favourable such that the Company is able to operate in a safe, efficient and effective manner; political and regulatory stability; the receipt of governmental, regulatory and third party approvals, licenses and permits on favourable terms; obtaining required renewals for existing approvals, licenses and permits on favourable terms; requirements under applicable laws; sustained labour stability; stability in financial and capital goods markets; availability of equipment; positive relations with local groups and the Company’s ability to meet its obligations under its agreements with such groups; and satisfying the terms and conditions of the Company’s current loan arrangements. While the Company considers these assumptions to be reasonable, the assumptions are inherently subject to significant business, social, economic, political, regulatory, competitive and other risks and uncertainties, contingencies and other factors that could cause actual actions, events, conditions, results, performance or achievements to be materially different from those projected in the forward-looking information. Many assumptions are based on factors and events that are not within the control of the Company and there is no assurance they will prove to be correct.

Furthermore, such forward-looking information involves a variety of known and unknown risks, uncertainties and other factors which may cause the actual plans, intentions, activities, results, performance or achievements of the Company to be materially different from any future plans, intentions, activities, results, performance or achievements expressed or implied by such forward-looking information. Such risks include, without limitation the risk factors listed under the heading “Risk Factors” in the Annual Information Form of the Company for the year ended December 31, 2018, dated March 14, 2019.

Although the Company has attempted to identify important factors that could cause actual actions, events, conditions, results, performance or achievements to differ materially from those described in forward-looking information, there may be other factors that cause actions, events, conditions, results, performance or achievements to differ from those anticipated, estimated or intended.

The Company cautions that the foregoing lists of important assumptions and factors are not exhaustive. Other events or circumstances could cause actual results to differ materially from those estimated or projected and expressed in, or implied by, the forward-looking information contained herein. There can be no assurance that forward-looking information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. Accordingly, readers should not place undue reliance on forward-looking information.

Forward-looking information contained herein is made as of the date of this press release and the Company disclaims any obligation to update or revise any forward-looking information, whether as a result of new information, future events or results or otherwise, except as and to the extent required by applicable securities laws.

GENERAL, Unless otherwise stated, information of a scientific or technical nature in respect of the Vale do Curaçá Property included in this press release is based upon the Vale do Curaçá technical report entitled “2018 Updated Mineral Resources and Mineral Reserves Statements of Mineração Caraíba’s Vale do Curaçá Mineral Assets, Curaçá Valley”, dated October 17, 2018 with an effective date of August 1, 2018, prepared by Rubens Jose De Mendonça, MAusIMM, of Planminas and Porfirio Cabaleiro Rodrigues, MAIG, Fábio Valério Cãmara Xavier, MAIG, and Bernardo Horta de Cerqueira Viana, MAIG, all of GE21 Consultoria Mineral, whom are independent qualified persons under NI 43-101. Information of a scientific or technical nature in respect of the NX Gold Mine included in this press release is based upon the Vale do Curaçá technical report entitled “Mineral Resource and Mineral Reserve Estimate of the NX Gold Mine, Nova Xavantina”, dated January 21, 2019 with an effective date of August 31, 2018, prepared by Porfirio Cabaleiro Rodrigues, MAIG, Leonardo Apparicio da Silva, MAIG, and Leonardo de Moraes Soares, MAIG, all of GE21 Consultoria Mineral, whom are independent qualified persons under NI 43-101.

Cautionary Notes Regarding Mineral Resource and Reserve Estimates In accordance with applicable Canadian securities regulatory requirements, all mineral reserve and mineral resource estimates of the Company disclosed or incorporated by reference in this press release have been prepared in accordance with NI 43-101 and are classified in accordance with the CIM Standards.

Mineral resources which are not mineral reserves do not have demonstrated economic viability. Pursuant to the CIM Standards, mineral resources have a higher degree of uncertainty than mineral reserves as to their existence as well as their economic and legal feasibility. Inferred mineral resources, when compared with Measured or Indicated mineral resources, have the least certainty as to their existence, and it cannot be assumed that all or any part of an Inferred mineral resource will be upgraded to an Indicated or Measured mineral resource as a result of continued exploration. Pursuant to NI 43-101, Inferred mineral resources may not form the basis of any economic analysis. Accordingly, readers are cautioned not to assume that all or any part of a mineral resource exists, will ever be converted into a mineral reserve, or is or will ever be economically or legally mineable or recovered.